In December, the Regional Church was shocked when we received the 2022 Insurance Premiums. The premiums have increased a lot! Several congregational leaders have called us asking “why is our insurance so high?”

Timothy S. Harris, President and CEO of the Insurance Board published this article in the Fall/Winter 2021 issue of The Steward. Here is the explanation in part: (Read the full article here.)

I’ve received inquiries from customers and agents alike as to why insurance premiums have increased during the pandemic. After all, many churches have not been conducting in-person services which some have translated to suggest fewer and less costly claims. Unfortunately, while the incidence of certain types of claims has reduced during the pandemic, the notion that the cost of claims has subsided is far from accurate. Property claim costs in 2020 were up 31% over 2019, on top of a 14.5% increase the prior year. In fact, despite the pandemic, 2020 property claims were among the highest in the Insurance Board Program’s history. Property claims at the end of 2020 were more than double the claim costs in 2015 yet we have not doubled the premiums charged to policyholders.

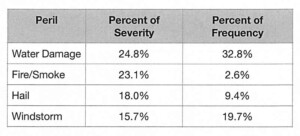

Additionally, during the pandemic, supply costs and materials used to repair damaged churches have increased. All of these factors add to the costs of claims. Premium costs charged in the Insurance Board Program are a direct function of the claim costs paid. Churches are experiencing more frequent and more costly claims. Because Insurance Board only serves churches and their affiliated ministries, these costs are all attributable to church claims. For the 6 years ending 12/31/2020, the top IB church property claims were as follows:

As the chart illustrates, water damage claims (frozen pipes, appliance leaks, sprinkler leakage, water intrusion from weather, sump pump failures, etc.) accounted for nearly a third of all property claims and more than a quarter of all property claim dollars spent. Over a six-year span, water damage claims alone have added an average of more than $1,000 per church, per year, or nearly 10% to insurance premiums. Water damage claims are largely preventable and are often the result of deteriorating infrastructure and lack of adequate maintenance.

We’ve all heard the axiom, “An ounce of prevention is worth a pound of cure.” This is especially true when it comes to church insurance. Some effort and, yes, cost expended on the front-end addressing building issues (leaky roofs and pipes, improper drainage, caulking, broken or clogged gutters and downspouts, etc.) can have a material impact on not only improving church properties, but also in significantly reducing insurance premiums. While not all insurance claims are preventable (the very reason insurance exists), many are, and others can be mitigated. Somewhere along the way, however, building maintenance has become less of a priority. I’ve heard parishioners say, understandably, that they want their stewardship going to missions, i.e., sheltering the homeless, feeding the poor, caring for the elderly, etc., all while the roof leaks, the walls are stained from water intrusion, the gutters need repaired, pipes and appliances are dripping. Yet, the church is often mission headquarters and the gathering space for God’s work and people. The risk management techniques communities of churches employ within their ministries (including resources that can be utilized at no charge) can go a long way in reducing the premiums this same community pays for insurance. Please reach out to us or visit our website to learn how you can improve risk at your ministry.